📸 Snapshot: Del Monte Pacific’s $1.2 Billion Restructuring Plan

The Campos family’s Del Monte Pacific is trying to rebuild its capital structure around its Philippine business.

On 1 July 2025, Del Monte Foods – the US subsidiary of Del Monte Pacific – announced that it would sell its assets in a court-supervised bankruptcy process as part of its agreement with a group of lenders.

I wrote on 2 July 2025 that Del Monte Foods’ “trapdoor” trick – dropping a set of collateral to an unrestricted unit that repledged those assets to get new loans – set off the chain reaction that led to its bankruptcy filing.

I noted that while the Campos family’s Del Monte Pacific would likely take a hit from the deconsolidation of Del Monte Foods, its cash-generating Philippine business had consistently outperformed the US subsidiary.

Del Monte Pacific announced on 31 July 2025 that it had recognized an asset impairment of USD 703.5 million related to the US operations.

On 1 August 2025, Del Monte Pacific Chief Financial Officer Parag Sachdeva reportedly told a conference call that the company was considering a listing of its profitable Philippine subsidiary to help cover the deficit.

Fast forward to the present and Del Monte Pacific – which is dual-listed on the Singapore Exchange and the Philippine Stock Exchange – has proposed a USD 1.2 billion restructuring.

So what happened along the way? The “capital and financial recovery plan” submitted by the group to both stock exchanges this week provides some context.

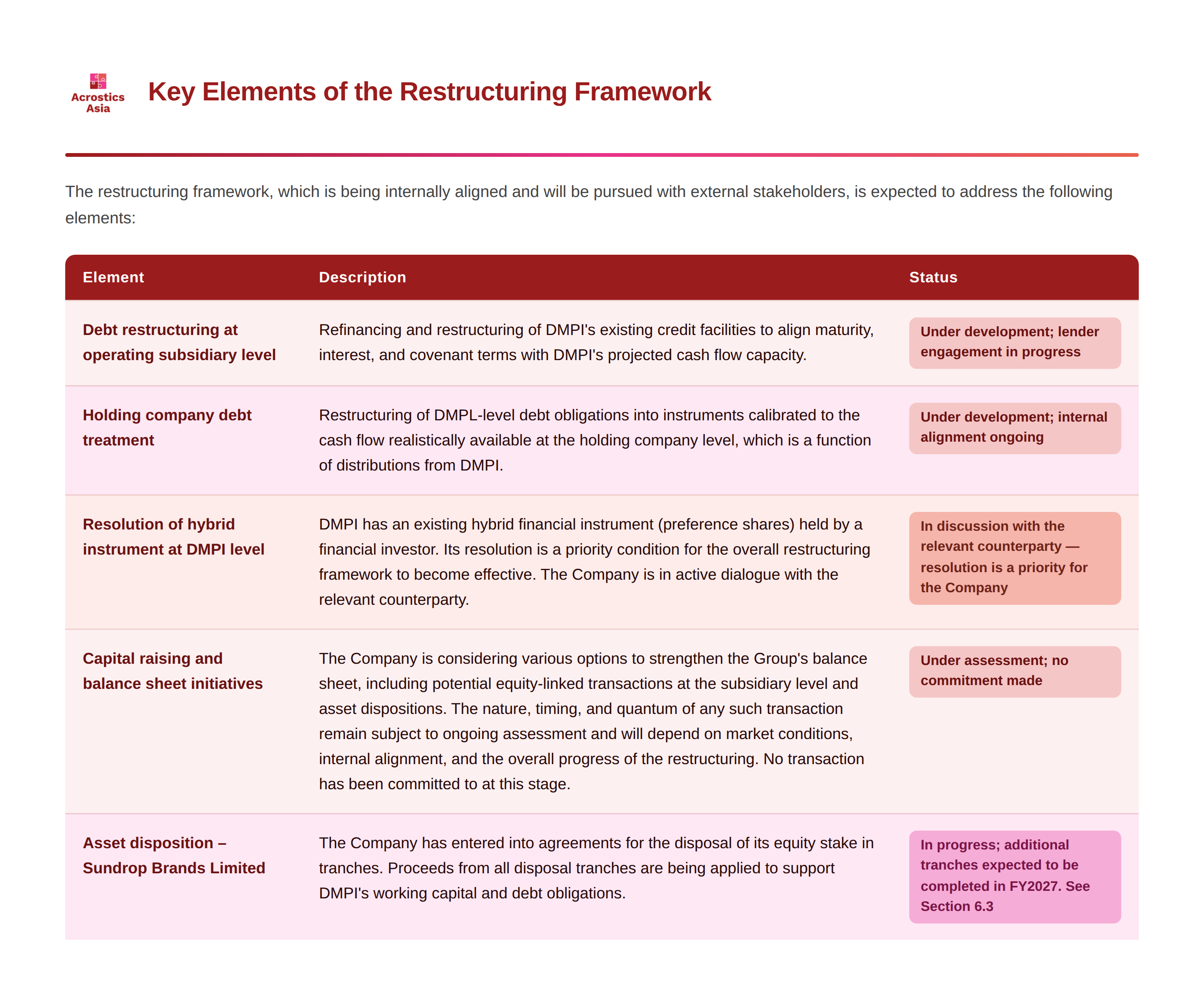

Restructuring Framework

Del Monte Pacific (DMPL) said that the bankruptcy of its former US subsidiary and the accounting consequences at the holding company level are “structural and non-recurring in nature”.

They do not reflect the underlying performance of the group’s continuing operations, which are anchored by Del Monte Philippines (DMPI), according to its restructuring plan.

Del Monte Pacific’s move to deconsolidate Del Monte Foods was likely aimed at preventing the US subsidiary from continually dragging down the group’s Philippine crown jewel. However, the company’s attempt to raise equity to plug the hole in its balance sheet did not seem to have gained traction so far.

“The Company is considering various options to strengthen the Group’s balance sheet, including potential equity-linked transactions at the subsidiary level and asset dispositions. The nature, timing, and quantum of any such transaction remain subject to ongoing assessment and will depend on market conditions, internal alignment, and the overall progress of the restructuring. No transaction has been committed to at this stage.”

Del Monte Pacific is now pursuing a comprehensive restructuring of the group’s capital structure.

“The total debt perimeter subject to the restructuring is approximately US$1.2 billion, spanning four entity levels within the Group structure. This includes the senior secured facilities at the DMPI operating level, holding company debt obligations at the DMPL level, and another debt facility associated with the S&W entity.”

Philippine Anchor

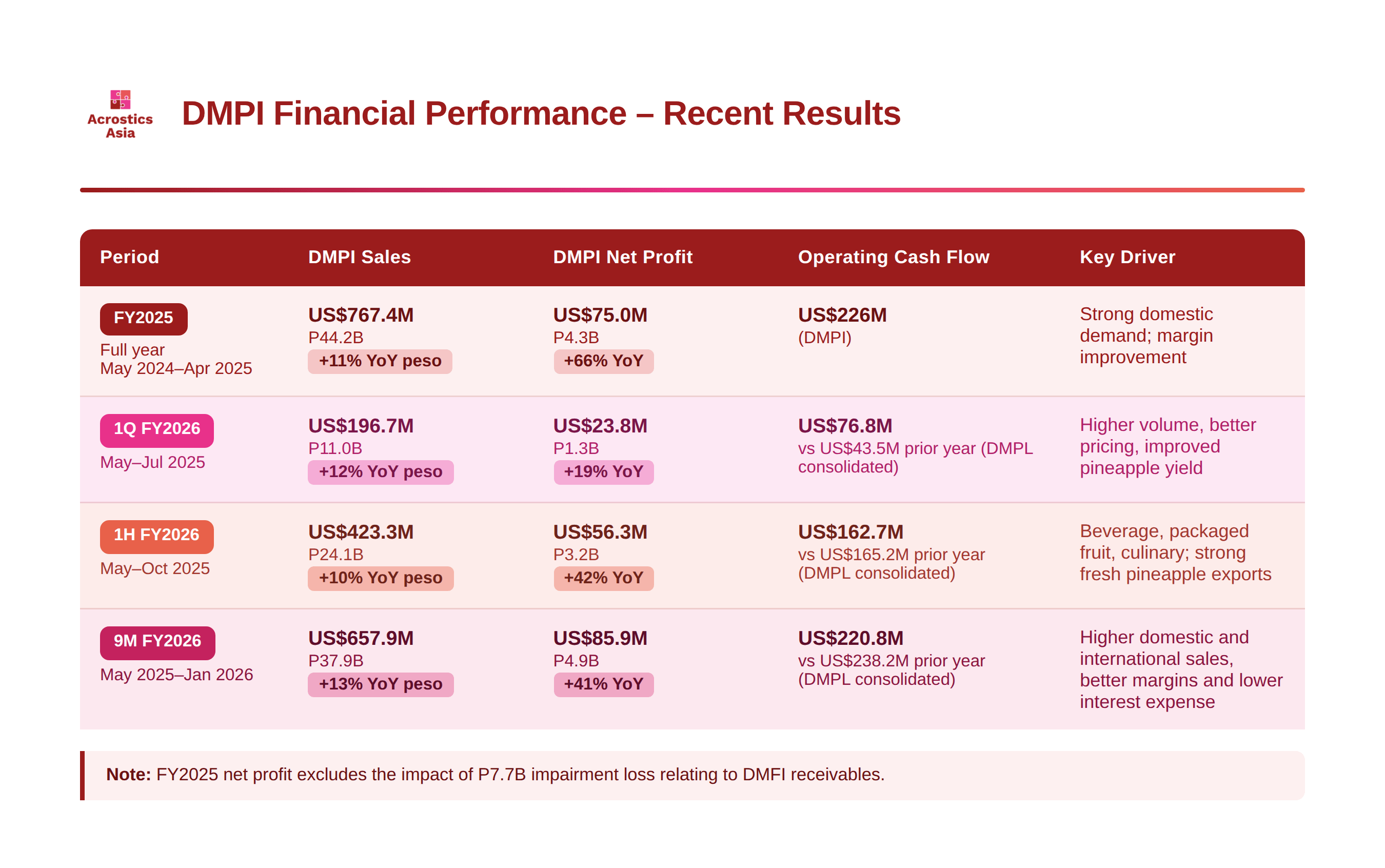

Del Monte Pacific emphasized that its Philippine subsidiary (DMPI) is “not in financial distress.”

“It continues to operate profitably with strong revenue growth, expanding margins, and robust operating cash generation. The difficulties are structural – at the DMPL holding company level – not operational.”

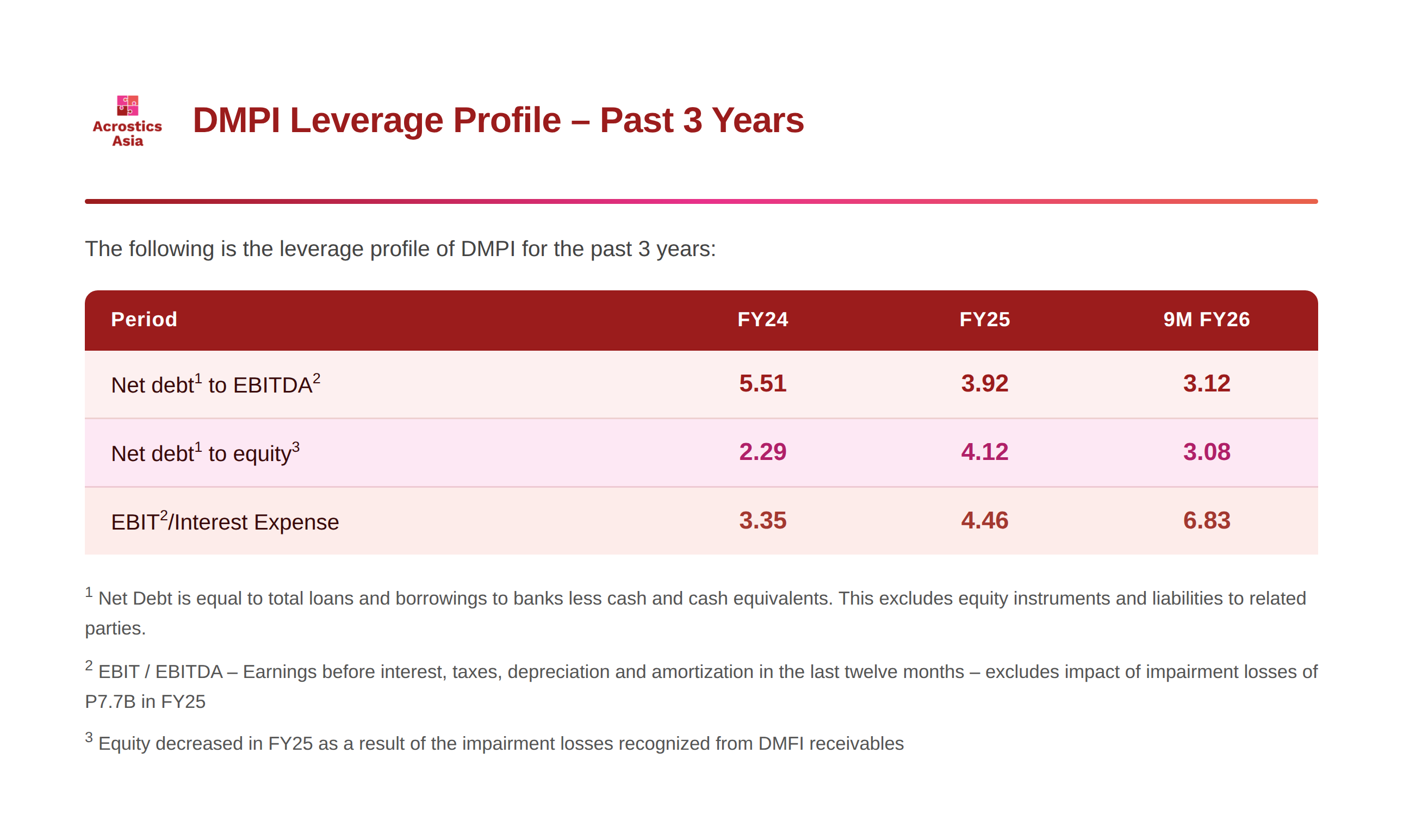

DMPI’s net debt to EBITDA has improved from 5.51 in FY24 to 3.12 in 9M FY26, while interest coverage (EBIT to interest expense) roughly doubled to 6.83 over the same period.

However, its equity decreased in FY25 as a result of impairment losses recognized from receivables owed by the US operating company.

“Fulcrum Event”

Del Monte Pacific’s restructuring plan was designed to pave the way towards DMPI’s refinancing by July or August 2027, which was described by the company as “the fulcrum event at which all obligations are resolved.”

However, this likely hinges on the resolution of DMPI’s preference shares that are held by a financial investor. “Its resolution is a priority condition for the overall restructuring framework to become effective,” Del Monte Pacific said, adding that the company is in “active dialogue with the relevant counterparty.”

In a nutshell, Del Monte Pacific is trying to rebuild its capital structure around its Philippine business, which remains the group’s primary cash engine but sits inside a highly leveraged holding framework.

The feasibility of the restructuring depends on whether it can get DMPI’s preference shares investor on board and sell the recovery story to the broader group of creditors.

Acrostics Asia Coverage

Acrostics Asia is an independent credit intelligence provider that delivers forward-looking insights across Asian sovereigns, private credit and restructurings.