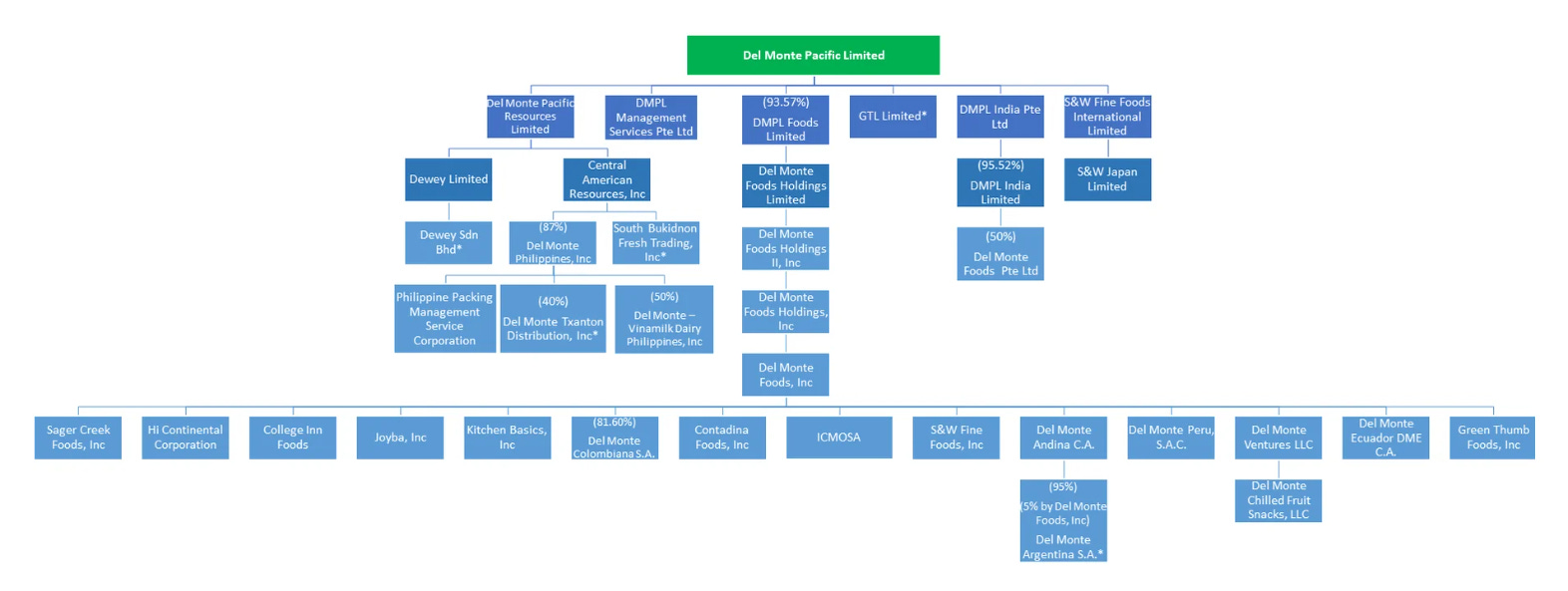

📚 Acrostics Anatomy: Del Monte’s Philippine Lifeboat

Del Monte Pacific’s Philippine unit rescued the Campos family’s flagship company after the loss of its US arm.

📒🎞️ Quick Take: Del Monte’s Fruity Drama (2 July 2025)

💼 Brief Take: Del Monte’s American Peel (4 July 2025)

📸 Snapshot: Del Monte’s Four Seasons (5 July 2025)

📒 Quick Take: Del Monte’s Ark (9 July 2025)

📒 Quick Take: A Tale of Two Del Montes (17 July 2025)

💼 Brief Take: Del Monte Pacific’s Revival Hope (2 August 2025)

📒 Quick Take: Del Monte’s Fruity Drama

2 July 2025

Del Monte Pacific’s US subsidiary initiated a court-supervised asset sale under the Chapter 11 bankruptcy proceedings.

The canned fruits producer’s “trapdoor” manoeuvre last year set off the chain reaction that resulted in lenders taking control of the US unit.

Del Monte has long been synonymous with canned fruits, but it’s also packed with corporate drama.

On 1 July 2025, Del Monte Foods – the US subsidiary of Del Monte Pacific – announced that it will sell its assets in a court-supervised bankruptcy process as part of its agreement with a group of lenders.

These are the key details in the press release:

Del Monte Foods has entered into a restructuring support agreement (RSA) with certain lenders, which set the stage for a sale of substantially all of its assets.

The company and its units initiated voluntary Chapter 11 proceedings in the US Bankruptcy Court for the District of New Jersey to implement terms of the agreement.

Del Monte Foods will have access to around USD 912.5 million of “debtor in possession” financing – including USD 165 million in fresh funds – to keep the operations running.

Philippine tycoon Joselito Campos’ Del Monte Pacific – which is dual-listed in Singapore and Manila – disclosed that it has lost control of its US subsidiary and is assessing the financial impact of the deconsolidation.

As of 31 January 2025, Del Monte Pacific’s net investment value in the US subsidiary was USD 579 million, while net receivables owed by Del Monte Foods and its units amounted to USD 169 million.

The Singapore-listed shares of Del Monte Pacific plunged more than 9% after the announcement, according to the Business Times.

So how did it come to this?

The Trapdoor

Last year, Del Monte Foods shifted most of the assets securing a USD 725 million loan to an unrestricted subsidiary, which then used those assets as collateral to get new “super priority” loans. This was basically a “trapdoor” or “drop-down” manoeuvre that was pioneered by US retailer J.Crew in its 2016 debt restructuring.

The lenders who were stripped of their key collateral then fought back. They replaced the original loan agent and declared that Del Monte Foods’ 2024 transactions had triggered events of default under the loan agreement.

Then their representative filed a lawsuit in the Delaware Court of Chancery to assert their rights to replace Del Monte Foods’ board of directors as a result of the default. Before the scheduled closing arguments, both sides reached a settlement in April 2025.

However, Del Monte Pacific announced on 5 May 2025 that it would not pay up to USD 45 million to the US subsidiary’s lenders, which was required under their settlement agreement. The lenders then seized control of Del Monte Foods and took 25% of Del Monte Pacific’s stake in the US subsidiary.

Del Monte Foods eventually filed for bankruptcy protection in the US and was deconsolidated from its parent company, but this is unlikely to be the end of the international soap opera.

💼 Brief Take: Del Monte’s American Peel

4 July 2025

Del Monte Pacific – the mothership of the Campos family’s food empire – will likely take a hit from the loss of its US arm, but its Philippine unit shouldn’t be as badly affected.

Del Monte Pacific’s debt stack included USD 70 million in perpetual securities.

🍑 Del Monte Foods, a 139-year-old company known for canned fruits and vegetables, filed for bankruptcy on 1 July 2025 as it seeks to sell its assets under a restructuring agreement with a group of lenders. Herbert Smith Freehills Kramer (US) LLP and Cole Schotz P.C. are the US company’s legal counsel, Alvarez & Marsal North America is its financial advisor, and PJT Partners is its investment banker.

🍑 I wrote that Del Monte tried to outsmart its lenders last year by dropping the collateral for a USD 725 million loan to an unrestricted unit, which re-pledged those assets to get fresh loans. However, this “trapdoor” trick backfired as the lenders who were deprived of their collateral then seized control of the US company. The law firm that devised this counterstrike operation was Friedman Kaplan, according to its press release.

🍑 How will the loss of the US arm affect the Del Monte empire? Philippine tycoon Joselito Campos’ Del Monte Pacific – the mothership that’s dual-listed in Singapore and Manila – said its auditor is assessing the value to be impaired. It’s not looking good, as the US subsidiary accounted for 72% of group sales for the 2024 financial year. Del Monte Pacific also had USD 579 million of net investment value in the US subsidiary as of 31 January 2025, while net receivables amounted to USD 169 million.

🍑 Nevertheless, Del Monte Pacific said its indirect subsidiary, Del Monte Philippines, continues to perform well on the back of resilient consumer demand and a stable supply chain. The unit, which is one of the largest F&B manufacturers in the Philippines, is expected to “maintain uninterrupted business operations going forward”, according to its statement.

🍑 Del Monte Pacific’s debt stack included USD 70 million in perpetual securities, which were issued in March 2024 by its indirect unit, Jubilant Year Investments, and guaranteed by Del Monte Philippines and Philippine Packaging Management Service Corporation. In 2020, Del Monte Philippines also raised PHP 6.47 billion (USD 114.5 million) in three-year and five-year local bonds.

📸 Snapshot: Del Monte’s Four Seasons

5 July 2025

A Philippine conglomerate’s expansion of its food empire to the United States through a debt-funded acquisition has turned out to be a disaster.

I broke it down into a four-part act.

A Philippine conglomerate’s expansion of its food empire to the United States through a debt-funded acquisition has turned out to be a disaster.

I wrote that Del Monte’s “trapdoor” trick last year backfired as its lenders launched a counterstrike operation and seized its US arm, culminating in the bankruptcy filing of the canned fruits and vegetables producer.

This is not the end of the 139-year-old brand as the Chapter 11 proceedings are likely intended to clean up the US company’s overly leveraged balance sheet and attract a new buyer. Still, the aggressive buyout more than a decade ago planted the seeds for the soured deal today.

The Original Sin

In October 2013, the Campos family’s Del Monte Pacific – which is dual-listed in Singapore and Manila – announced that it would acquire the consumer food business of privately owned Del Monte Foods in a USD 1.675 billion deal. The US business was churning out USD 1.8 billion of sales, USD 178 million of adjusted EBITDA, and healthy cashflows at the time.

“Prior to this acquisition, the U.S. was one of few key markets where our Company did not have a direct presence nor have its own brands,” Del Monte Pacific Chairman Rolando Gapud said in the statement.

However, the target company ended up being saddled with much of the debt that funded the acquisition. This was the breakdown of the debt component (check out the list of advisers for the deal on page 5 of the PDF here):

The Rot

Del Monte Foods had to make escalating debt payments even as its core business was declining due to the shift of consumer spending towards healthier alternatives. The company also made a mis-step by committing to peak production volumes during the Covid-19 bump, which resulted in excess inventory after the pandemic subsided.

In court documents supporting Del Monte Foods’ Chapter 11 filing, Chief Restructuring Officer Jonathan Goulding laid out the cost of servicing its debt:

“The Company has carried substantial funded indebtedness since its acquisition by DMPL (Del Monte Pacific) in 2014, whereby DMPL placed debt on the Company to fund its acquisition. Over time, as the capital structure has been refinanced, interest rates have continued to increase, and the Company’s annual cash interest expense went from approximately $66,000,000 in Fiscal Year 2020 to $125,000,000 in Fiscal Year 2025, which significantly constrained the Company’s liquidity.”

Del Monte Pacific also chose not to pay USD 45 million under its settlement with the group of lenders who challenged its “trapdoor” transactions. Goulding disclosed that the skipped payment had a domino effect on the US subsidiary’s arrangements with its vendors.

“Altogether, this perfect storm of reduced margins, excess inventory and decreased customer demand created an unprecedented liquidity crisis for the Company. To manage its liquidity, the Company has historically (and increasingly in recent years) relied on favorable trade terms with its vendors and has stretched vendor payments, resulting in substantial accounts payable, some of which is subject to contractual penalties and interest. On May 5, 2025, DMPL publicly announced that it was declining to make the $45,000,000 equity investment in the Company under the Transfer Agreement. In the wake of this announcement, the Company’s vendors began to contract trade terms, which in turn further reduced the Company’s liquidity. It was at this point, as discussed further herein, that the Company began discussions with its stakeholders on the terms of a potential restructuring.”

Cain & Abel

Back on the mothership, the bosses were not hiding their view that the American business was dragging down its sister company Del Monte Philippines.

Del Monte Pacific also emphasized that Del Monte Philippines remains strong despite the bankruptcy filing of the US company. “Del Monte Philippines Inc (DMPI), with its Asian and international businesses, continues to perform well with resilient consumer demand, supported by a strong and stable supply chain,” it said.

On a side note, my Yoda Richard Borsuk pointed out that in 2005, Indonesian conglomerate Salim Group’s investment arm First Pacific tried to buy into Del Monte Pacific’s pineapple plantations in the Philippines, but the deal didn’t come to fruition. (Check out his biography of the late founder of Salim Group, which is another fascinating Asian conglomerate).

Fresh Start

The accountants are crunching the numbers on the impact of losing the US arm, but perhaps Del Monte Pacific was already drawing the line on the sand by choosing not to pay USD 45 million to the lenders. After cutting the US losses, the flagship company is likely to focus on shoring up its Asian base via Del Monte Philippines.

In the US, Del Monte Foods President and CEO Greg Longstreet said a court-supervised sale process is the most effective way to accelerate its turnaround. “With an improved capital structure, enhanced financial position and new ownership, we will be better positioned for long-term success,” he said.

Breaking up was probably hard to do because no one wanted to admit that the 11-year marriage was a mistake, but it’s likely for the best.

📒 Quick Take: Del Monte’s Ark

9 July 2025

Del Monte Pacific’s Philippine unit can potentially be a lifeboat for the Campos family’s flagship company after losing its US arm.

Del Monte Pacific might be able to raise funds to plug its deficit, especially if there’s a guarantee from its Philippine crown jewel.

Del Monte Pacific’s Philippine unit can potentially be a lifeboat for the Campos family’s flagship company to navigate choppy waters after losing its US arm.

Last week, California-based Del Monte Foods initiated Chapter 11 proceedings to clean up its balance sheet and sell its assets to a new buyer. A group of lenders also appointed a majority of directors to the board of Del Monte Foods and took 25% of Del Monte Pacific’s equity in the US company.

Balance Sheet Hole

There’s no sugar-coating the fact that Del Monte Pacific will take a hit from the deconsolidation of its US subsidiary.

Del Monte Pacific had USD 579 million of net investment value and USD 169 million of net receivables tied to Del Monte Foods, which are subject to an impairment. These write-offs are likely to cause a capital deficit in Del Monte Pacific’s balance sheet, according to its response to a query from the Singapore Exchange.

Without the US subsidiary, current liabilities exceeded current assets by USD 595 million at a group level and USD 382 million at Del Monte Pacific’s level as of 30 April 2025. “This is mainly driven by the loans of the Philippine subsidiary, Del Monte Philippines, being of a revolving nature as prescribed by local banking partners,” Del Monte Pacific said.

These revolving loans were likely classified as short-term debt and contributed to the deficit, even though the company may have consistent access to the credit line. The long-term loans – including amortizations – of Del Monte Pacific and its Philippine subsidiary should also be refinanced or extended, the company said, adding that it has secured an extension from a major lender.

Del Monte Pacific reported USD 1.17 billion in current liabilities as of 31 January 2025, out of which USD 693.2 million were in the form of loans and borrowings, according to its latest results. Short-term unsecured loans accounted for 70.5% of these loans and borrowings. (For the terms and debt repayment schedule, check out page 35 of the PDF here).

Philippine Crown Jewel

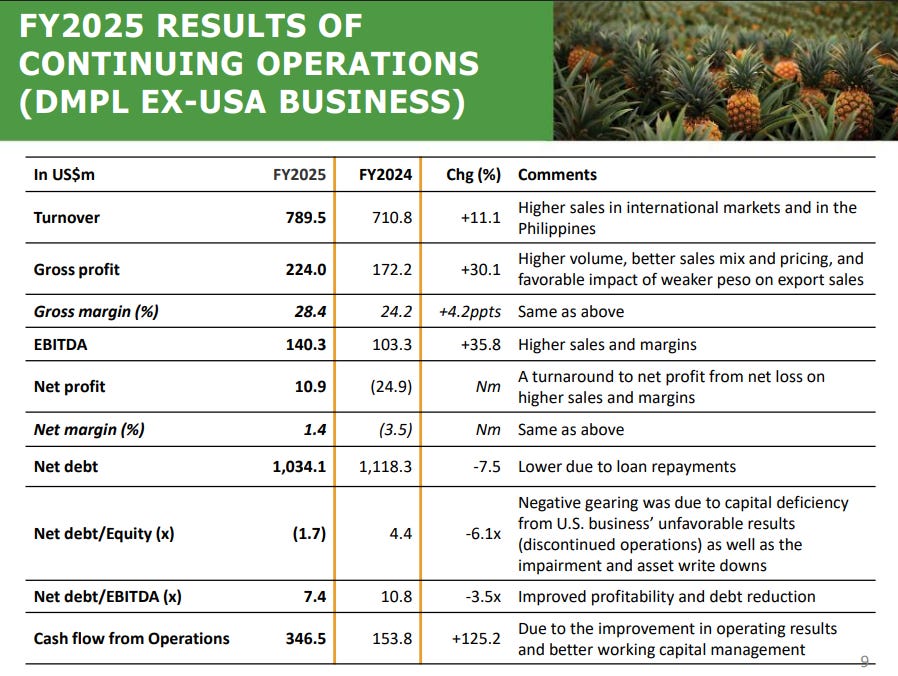

The good news is Del Monte Pacific has received dividends from its Philippine subsidiary, which generated USD 226 million of positive cashflow in its 2025 financial year. “Management has been pursuing equity raising initiatives as the Group’s Asian operations has restored profitability,” Del Monte Pacific said.

Del Monte Philippines reported a 14% increase in sales to PHP 44.2 billion (USD 783.7 million) for the year ended in April 2025, driven by exports of fresh pineapples and packaged products, according to its press release. Over the same period, EBITDA jumped 40% to PHP 8.6 billion (USD 152.5 million).

Del Monte Pacific might be able to raise funds to plug its deficit, especially if there’s a guarantee from its Philippine crown jewel.

📒Quick Take: A Tale of Two Del Montes

17 July 2025

Consumers favour natural food over canned preservatives, as shown by the diverging fortunes of two Del Montes.

Del Monte Foods will have to adapt its products to emerge out of bankruptcy, while Fresh Del Monte seems to be a well-run business set for more growth.

Fresh fruits are beating canned fruits to a pulp as consumers increasingly favour natural food over canned preservatives. This trend is not just seasonal, as illustrated by the diverging fortunes of two Del Montes.

Del Monte Foods, the California-based subsidiary of the Campos family’s Del Monte Pacific, initiated court-supervised bankruptcy proceedings on 1 July 2025 to clean up its balance sheet and sell its assets. On the other hand, Florida-based Fresh Del Monte is emerging as an investors’ darling on the back of its strong results and product positioning.

While both businesses share rights to the Del Monte name through historical licensing arrangements, they operate under distinct ownership and serve different geographic markets, according to Fresh Del Monte’s statement. “The two companies are entirely separate entities, with no shared ownership, governance, or operations.”

🥫 Canned Fruits

The seeds of Del Monte Foods’ downfall were planted when it was acquired by Del Monte Pacific in 2014 and loaded with the debt that funded the aggressive buyout.

However, the US company was also responsible for several operational mis-steps, such as a mismatch between its inventory build-up and the ebbing demand for canned food post pandemic.

On the products front, Del Monte Foods is neither here nor there: The brand doesn’t resonate enough with higher-end shoppers to justify a premium pricing, but it struggles to compete with cheaper private labels for prepared food in the US. It also doesn’t have the branding rights to fresh or fresh-cut fruits, limiting its ability to expand into this growth sector.

The company transferred some assets to an unrestricted subsidiary and offered the collateral to get additional loans last year, but this “trapdoor” trick angered a group of creditors and set the stage for its eventual bankruptcy filing.

While Del Monte Foods had lined up USD 165 million in new money as part of a USD 912.5 million debtor-in-possession (DIP) financing package, a portion of its existing debt was also rolled into this facility and the recovery for creditors is uncertain given the persistent headwinds.

🍈 Fresh Fruits

The story couldn’t be more different for Fresh Del Monte.

Institutional investors including Edgestream Partners and Gamma Investing raised their stakes in the fresh fruits company during the first quarter of this year (1Q25), according to a market report. Other shareholders in Fresh Del Monte reportedly include New York State Teachers Retirement System, Waterfront Wealth and CWA Asset Management Group.

These investors were likely attracted to Fresh Del Monte’s financial and operational health, as indicated by its latest results. Fresh Del Monte reported slightly lower net sales in 1Q25 because of a drop in its bananas segment and forex fluctuations, but it was able to squeeze out more earnings thanks to favourable margins and cost controls.

Unlike the highly leveraged Del Monte Foods, Fresh Del Monte is generating cash from its operations while actively reducing its debt and managing its capital spending.

There should still be space in supermarket shelves for canned food, but Del Monte Foods will likely have to keep up with the times and adapt its products to what shoppers want. Meanwhile, Fresh Del Monte seems to be a well-run business with a balanced product mix and cost controls, so it’s likely poised for more growth.

💼 Brief Take: Del Monte Pacific’s Revival Hope

2 August 2025

The Campos family’s Del Monte Pacific has chopped off a rotting arm to save the body, as its latest results showed that losses at the US business had ballooned.

A successful listing for Del Monte Pacific’s Philippine subsidiary can help to heal its wound.

Del Monte Pacific – the canned food producer controlled by Philippine tycoon Joselito Campos and his siblings – reported a record net loss of USD 834.4 million for its fiscal year ended April 2025, Forbes reported on 1 August.

Eveline’s Take:

🍏 The Campos family’s flagship company Del Monte Pacific has chopped off a rotting arm to save the body. This is laid bare in the Singapore-based company’s latest results: Before it was deconsolidated, the US subsidiary – Del Monte Foods – reported a post-tax loss of USD 892.4 million for the fiscal year ended 30 April 2025, eight times the USD 111.9 million loss a year earlier.

🍏 Del Monte angered a group of lenders last year when it shifted a set of loan collateral to an unrestricted subsidiary and then repledged the assets to get fresh loans. As part of its settlement with these lenders, Del Monte Pacific agreed on 9 April 2025 to either contribute up to USD 45 million as a subordinated loan to Del Monte Foods’ operating unit by 5 May 2025, or give up part of its equity in the US company.

🍏 However, Del Monte Pacific said that it ruled out additional funding due to the challenging US economy, the losses and constrained access to financing at the US unit, as well as the need to prioritize the group’s liquidity and support for its Philippine subsidiary. Subsequently, the lenders took control of Del Monte Foods and initiated bankruptcy proceedings in the US to squeeze out some recovery.

🍏 I wrote in early July that Del Monte Pacific would take a hit from the deconsolidation of its US subsidiary, but its cash-generating Philippine crown jewel can help to plug its deficit. Del Monte Pacific announced on 31 July that it had recognized a full impairment of USD 703.5 million related to the US business. But the group expects to be profitable in FY2026, driven by its Philippine unit.

🍏 Del Monte Pacific’s non-US business delivered a strong performance in FY2025, with growth across the board – including turnover, gross profit, profit margins, EBITDA and operating cashflow – while net debt declined on loan repayments. Del Monte Pacific Chief Financial Officer Parag Sachdeva said in a conference call on 1 August that the company is considering a listing of its Philippine subsidiary to cover the deficit from its US operations, Forbes reported.

🍏 I wrote last month that the Philippine unit can be a lifeboat for Del Monte Pacific to steady itself after cutting its US arm adrift. A successful listing for Del Monte Philippines can potentially pull its parent company out of the choppy waters.